How to Determine Your Current Financial Status – Are you ready to take control of your financial future? Personal finance may seem daunting, but understanding where you stand is the first step toward financial freedom. Let’s dive into personal finance together and discover how knowing your financial situation can pave the way for a more secure tomorrow.

The Importance of Knowing Your Financial Situation

Understanding your current financial situation is crucial in making informed decisions about your money. By clearly showing where you stand financially, you can identify areas for improvement and set realistic goals.

Knowing how much money you have coming in and going out each month allows you to track your spending patterns and make necessary adjustments. This awareness helps prevent overspending and ensures you live within your means.

Evaluating your debt levels and savings account balances gives insight into your financial health. It lets you prioritize paying off high-interest debt and building emergency funds for unexpected expenses.

Setting specific financial goals becomes easier when you have a solid understanding of your current situation. Whether saving for a down payment on a house or planning for retirement, knowing your starting point is essential for creating an effective strategy.

Knowing your financial situation empowers you to manage your money and work towards a more secure future.

How to Determine Your Current Financial Status

Understanding your current financial status is crucial in making informed decisions about your money. To determine where you stand financially, gather all your financial documents, such as bank statements, bills, and investment accounts. This will give you a clear picture of your income sources and expenses.

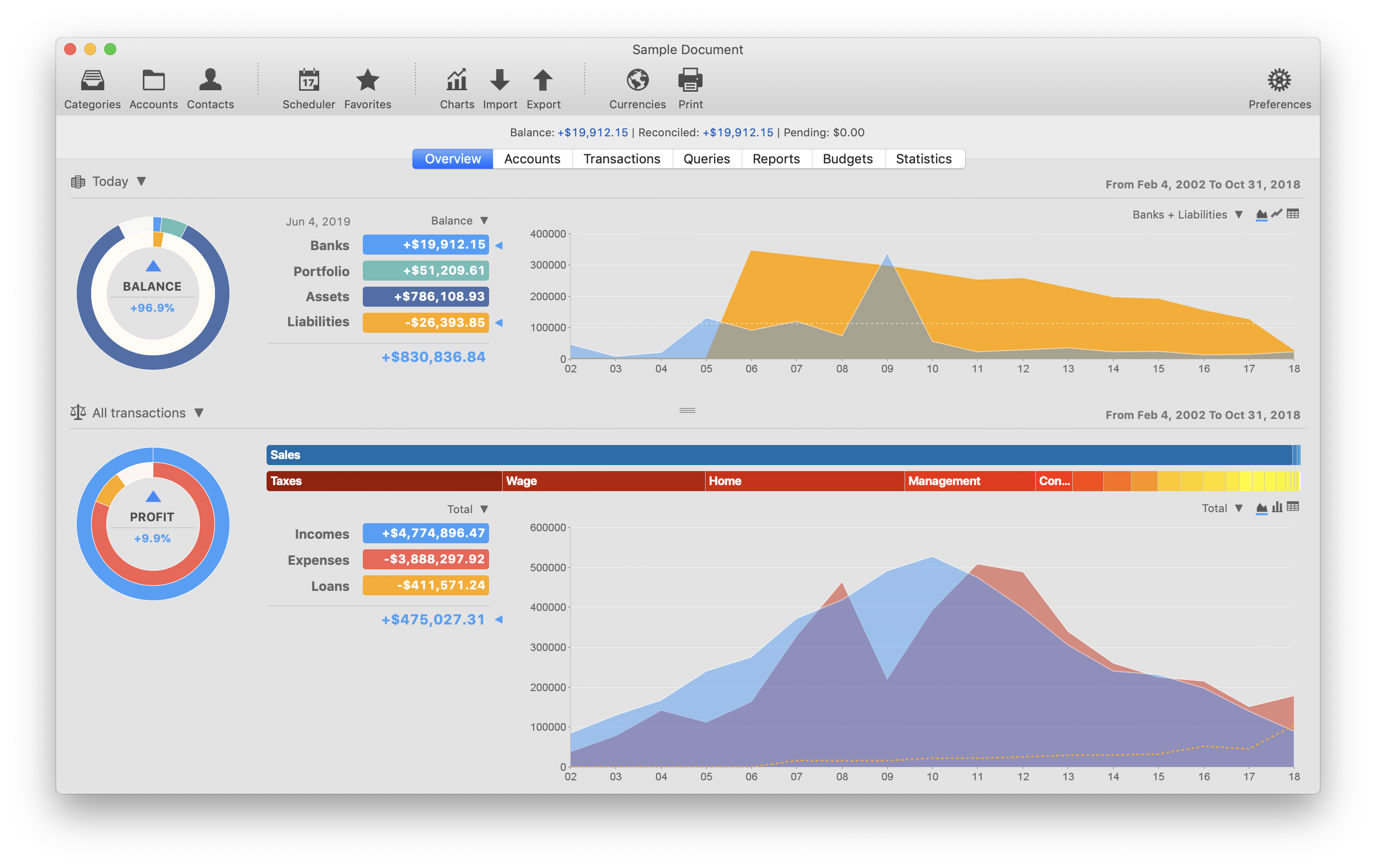

Next, calculate your total assets with personal finance software like iCash by entering the value of everything you own, such as savings accounts, investments, real estate properties, and personal belongings. Then, enter your liabilities—debts and loans—to get a net worth figure.

iCash helps you evaluate how much debt you have compared to your savings. High-interest debts can hinder financial progress, while having substantial savings provides security for unexpected expenses or future goals.

It is also essential to assess how well you meet short-term and long-term financial goals. Are you saving enough for retirement? Do you have an emergency fund?

By understanding these aspects of your finances, you can make informed choices about budgeting effectively and setting achievable financial objectives based on your current financial situation.

Tracking Income and Expenses

Tracking income and expenses is crucial to managing personal finances effectively. By recording how much money you earn and where it goes, you can gain insights into your spending habits and make informed decisions about your finances.

Start by tracking all income sources, whether from your job, side gigs, or investments. This will give you a clear picture of your monthly income.

Next, categorize your expenses – from fixed costs like rent and utilities to variable expenses such as groceries and entertainment. Tracking these expenditures will help you identify areas where you may be overspending or where you can cut back.

Consider using tools like iCash to streamline the process and make it easier to monitor your financial transactions regularly.

Remember that tracking income and expenses is not just about recording numbers; it’s about gaining control over your financial situation and working towards achieving your goals.

Evaluating Debt and Savings

Evaluating Debt and Savings is crucial to understanding your current financial situation. Regarding debt, take stock of all outstanding balances, interest rates, and monthly payments. This will give you a clear picture of how much you owe and to whom.

Next, assess your savings – both short-term and long-term. Determine your savings in emergency funds, retirement accounts, or other investments. Knowing your savings can help you gauge your financial stability and plan for future expenses.

Compare the amount of debt against your savings to see if you’re on track with your financial goals. If debt outweighs savings, it may be time to reevaluate your spending habits and prioritize paying off debts.

By evaluating debt and savings carefully, you can make informed decisions about where to allocate your resources effectively for a more secure financial future.

Setting Financial Goals

Setting financial goals is a crucial step in managing your finances effectively. It gives you direction and motivation to work towards achieving specific milestones.

Start by identifying what you want to accomplish financially, whether saving for a house, paying off debt, or investing for retirement. Be realistic yet ambitious with your goals.

Consider setting short-term and long-term goals to keep yourself on track and celebrate small victories. This will help maintain momentum and focus on your financial journey.

Make sure your goals are measurable to track your progress over time. Whether increasing your savings rate by a certain percentage each month or reducing credit card debt by a specific amount, having quantifiable targets keeps you accountable.

Revisiting and adjusting your financial goals regularly as circumstances change is essential. Stay flexible and adaptable to ensure your objectives remain relevant and achievable in the long run.

Creating a Budget Plan based on your Financial Situation

You’ve taken the critical step of assessing your financial situation. It’s time to create a budget plan tailored to your needs and goals.

Start by listing all your sources of income using personal software like iCash. This includes your salary, side hustles, rental income, or other regular money.

Next, track all your expenses meticulously. Every penny counts from fixed costs like rent and utilities to variable expenses like dining out or entertainment.

Evaluate where you can cut back on unnecessary spending. Maybe it’s eating out less frequently or finding more cost-effective ways to enjoy leisure activities.

Set realistic financial goals based on your current situation – saving for an emergency fund, paying off debt, or investing for the future.

Allocate funds in your budget plan to prioritize these goals while still covering essential expenses and enjoying life within your means.

Remember that creating a budget is not about restriction but rather about empowerment and taking control of your finances.

Seeking Professional Help for Better Understanding

Securing professional help with personal finance can provide valuable insights and guidance. Financial advisors or planners have the expertise to analyze your financial situation objectively and offer tailored solutions.

A professional can help you understand complex financial concepts, identify areas for improvement, and set achievable goals. They can assist in creating a personalized budget plan based on your current financial status and future aspirations.

Having a professional by your side can give you peace of mind, knowing you are making informed decisions about your money. They can also provide ongoing support and adjustments to keep you on track towards financial stability.

Don’t hesitate to contact a qualified expert for assistance with managing your finances effectively. Their knowledge and experience could make a significant difference in helping you achieve your financial goals.

In conclusion, how to Determine Your Current Financial Status?

Personal finance is a crucial aspect of life that requires attention and careful planning. By understanding your current financial situation, you can make informed decisions about budgeting, saving, and investing. Tracking income and expenses, evaluating debt and savings, setting financial goals, and creating a budget plan based on your financial situation are all steps that can help you take control of your finances.

Use a personal finance tool like iCash to streamline the process and make it easier to monitor your financial transactions. With the proper knowledge and iCash, you can confidently navigate the world of personal finance and set yourself up for a secure financial future. Take charge of your finances today to pave the way for a better tomorrow!

Related – What is Personal Finance Software and how iCash can help

Español:

Français: